2024-01-20

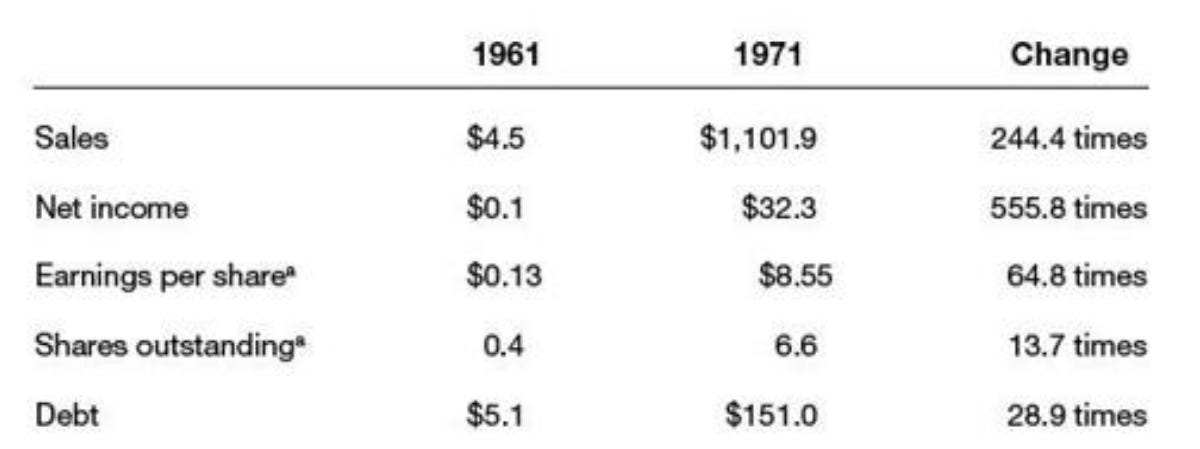

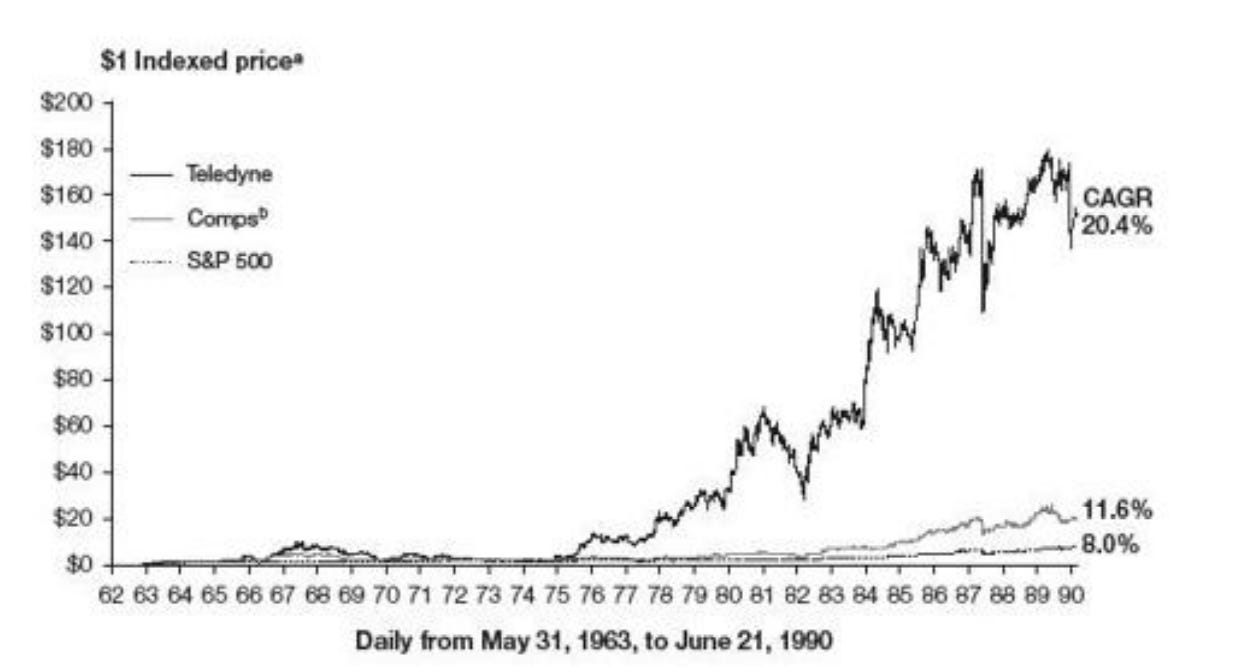

Henry Singleton graduated from MIT in 1950 and began working at Litton Industries, where he built the first inertial guidance system. After climbing the corporate ladder to become the general manager, he resigned in 1960 and, at the age of 43, founded Teledyne. Between 1961 and 1969, Singleton embarked on an ambitious acquisition spree, purchasing 130 companies across various industries, including aviation electronics, specialty metals, and insurance. Notably, the competitive landscape was favorable as there was minimal private equity involvement, and the acquired companies often had substantially lower P/E ratios than Teledyne's own.

The acquisition spree came to a halt in 1969 as Teledyne's P/E ratio declined, and acquisition prices rose. Singleton's strategic approach and principles played a key role in the success of Teledyne during this era.

As you can see, he still issued shares in these ten years, but while the shares only grew 14 times, his EPS grew 65 times. Like Tom Murphy, Singleton bet heavily on decentralization instead of 'integrations' and 'synergy.' He broke the companies into their smallest parts and drove accountability and managerial responsibility as far down the company as possible. 'Managers who made their numbers did well; those who did not moved on.'

He also, like Murphy, focused on cash flow instead of reported earnings.

Singleton and CFO Jerry Jerome built Teledyne's return to keep incentives high and focus on cash generation. These are the steps:

Bonus Compensation for Business Unit Managers based on Teledyne return.

After 1969, they:

Result: Huge cash generation and a high return on assets (20%).

When a division did not meet Teledyne standards and there was no turnaround in sight, they simply exited the industry. In 1972, Singleton initiated a tender and continued to buy back shares for the next 12 years, which was highly unusual for that time. In total, he repurchased more than 90% of the company's shares. Buybacks need to be strategically used; you cannot just repurchase whenever you want. In total, he brought back $2.5 billion in sizes ranging from 4% to 66% of book value, all at remarkably low P/E ratios while revenues and net income continued to grow. Teledyne issued stock over a P/E of 25 and repurchased below 8

In a bold contrarian move, he also increased the total equity allocation in the insurance portfolio from 10% to 77% in six years, investing 70% of the assets in only five companies, with 25% allocated to one specific company. He invested in companies he knew well (Curtiss-Wright, Texaco, Aetna) with record-low P/E ratios.

When Teledyne’s operating results started to decline, he began to spin off Argonaut and Unitrin to reduce complexity and unlock the full value of the company's operations. Fayez Sarofim stated, 'There was a time to conglomerate and a time to deconglomerate.' In 1997, not knowing what to do with his capital at high P/Es, he started to pay a dividend. Singleton retired as chairman in 1991.

Another important point for CEOs is time management. They can focus on the management of operations, capital allocation, and investor relations. Henry Singleton said, 'I don’t reserve any day-to-day responsibilities for myself, so I don’t get into any particular rut. I do not define my job in rigid terms but in terms of having the freedom to do whatever seems to be in the best interests of the company at any time.

'I know a lot of people have very strong and definite plans that they’ve worked out on all kinds of things, but we’re subject to a tremendous number of outside influences, and the vast majority of them cannot be predicted. So my idea is to stay flexible.'

'My only plan is to keep coming to work. . . . I like to steer the boat each day rather than plan ahead way into the future.'"

Like i said before much of this is taken from the book The Outsiders.

Thanks,

Finn